You’ll sometimes see references to Medicare Part C. This is just another name for Medicare Advantage, which is an all-in-one alternative to Original Medicare — meaning it replaces Medicare Part A (hospital coverage), Medicare Part B (medical insurance) and often Medicare Part D (drug coverage).

Medicare Part C plans are offered by private companies that have been approved by Medicare. Most plans provide benefits that aren’t covered under Original Medicare, such as dental, hearing and vision coverage. There may even be coverage for fitness programs (such as gym memberships), transportation to medical visits and over-the-counter drugs. Some plans also offer benefits tailored to certain chronic conditions.

» How to compare Medicare Advantage Plans

Medicare Part C comes in several types, much like non-Medicare health insurance, with different requirements for finding care providers. In an HMO plan, for instance, you need to see in-network health care providers unless it’s an emergency, and you need a referral to see a specialist. In a PPO plan, you can see both in-network and out-of-network health care providers, although you typically pay more to go out of network.

Companies offering Medicare Part C must follow certain regulations set by federal and state law, but out-of-pocket costs and rules for accessing services may differ from plan to plan, and companies can change those aspects from year to year. Compare each plan’s rules, benefits and costs before choosing one that’s right for you.

Advantages of Medicare Part C:

Instead of having Medicare Part A, B and D, you’ll have all coverage bundled into one plan.

There are typically extra benefits available, such as dental, vision and hearing coverage.

Your out-of-pocket costs could be lower than with Original Medicare.

You still receive all the rights and protections of Medicare.

Disadvantages of Medicare Part C:

Your list of in-network health care providers may be smaller than with Original Medicare.

You may have to get referrals or authorizations for some services, depending on your plan type.

Your plan may not cover you if you travel outside your service area.

To sign up for a Medicare Advantage Plan, you must have Original Medicare Part A and Part B coverage. Use Medicare’s Plan Finder to find and compare plans in your area.

When you can sign up

You can sign up for a Medicare Advantage (Part C) Plan at the following times:

During your initial enrollment period.

During each year’s fall open enrollment period, Oct. 15 to Dec. 7.

Between Jan. 1 and March 31 if you have Part A coverage and you get Part B for the first time.

If you’re already enrolled in a Medicare Advantage Plan, you can switch plans during the fall open enrollment period or during the Medicare Advantage open enrollment period from Jan. 1 to March 31.

As with most health care plans, Medicare plans have an annual open enrollment period. During this time, current Medicare users get a chance to evaluate their coverage and potentially make changes.

Medicare has one main open enrollment window from Oct. 15 to Dec. 7 each year. However, there’s also a Medicare Advantage open enrollment period annually from Jan. 1 to March 31.

What is Medicare open enrollment?

Open enrollment is the health care user’s chance to evaluate the plan they have, take a look at what’s on the market and update their coverage for the coming year. Open enrollment is for consumers who already have Original Medicare or Medicare Advantage.

During the main open enrollment period, from Oct. 15 to Dec. 7, any changes you make will take effect on Jan. 1. During the Medicare Advantage open enrollment period, any changes you make will take effect on the first of the month after the plan receives your request.

What you can change

There are several things you can alter during open enrollment. From Oct. 15 to Dec. 7, you can do the following things:

Switch from Original Medicare to a Medicare Advantage Plan.

Switch from a Medicare Advantage Plan back to Original Medicare.

Move from one Medicare Advantage Plan to a different one.

Join a Medicare prescription drug plan.

Switch from one Medicare prescription drug plan to another one

Drop your Medicare prescription drug coverage

From Jan. 1 to March 31, Medicare Advantage open enrollment, you can do the following things:

Switch from one Medicare Advantage Plan to another.

Quit your Medicare Advantage Plan and go back to Original Medicare, with the option to join a Medicare Prescription Drug Plan.

While it’s possible to switch from a Medicare Advantage Plan and go back to Original Medicare during both periods, it’s only possible to do the reverse (move from Original to Advantage) from Oct. 15 to Dec. 7.

Comparing Original Medicare and Medicare Advantage

If you have an Original Medicare plan — you’re enrolled in Medicare Part A and Medicare Part B — open enrollment is the time when you might consider switching to a Medicare Advantage Plan. For some people, purchasing a Medicare Advantage Plan feels simpler.

“Some people prefer the sense of a one-stop shop,” says Deborah Gordon, author of “The Health Care Consumer’s Manifesto: How to Get the Most for Your Money.” “Like, ‘I cannot deal with A, B, D, I just want a health plan.’”

Here’s what you should know:

Medicare Advantage Plans offer all the benefits of Part A and Part B. You won’t get less coverage with an Advantage plan.

Most Medicare Advantage Plans provide prescription drug coverage. If you stick with Original Medicare, you’ll have to sign up for Medicare Part D for prescription drug coverage.

Medicare Advantage Plans usually offer coverage for things that aren’t included under Original Medicare, such as dental, vision, hearing and wellness programs.

With a Medicare Advantage Plan, you must use health care providers that are in the plan’s network, and you may need a referral to see a specialist. With Original Medicare, you can use any health care provider in the United States that takes Medicare, and you usually won’t need a referral.

Some Medicare Advantage Plans may include lower out-of-pocket costs than Original Medicare. Original Medicare users may have to purchase supplemental coverage to help cover out-of-pocket costs.

Under Original Medicare, there is no limit on your out-of-pocket costs each year. With a Medicare Advantage Plan, once you spend a certain amount, the plan will cover 100% of the costs for the rest of the year.

While neither plan covers you if you travel outside of the U.S., you may be able to purchase a supplemental policy that would cover you in a foreign country if you have Original Medicare. Under Medicare Advantage, you can’t purchase any supplemental coverage plans.

How to compare Medicare Advantage Plans

Choosing a Medicare Advantage Plan can be a little intimidating because there are so many plans available. “The average Medicare beneficiary has something like two dozen choices,” Gordon says. “That seems great, like, ‘Oh, you have so many options,’ but it can be really overwhelming to consumers.”

There are five different types of Medicare Advantage Plans:

Health Maintenance Organization, or HMO, plans: This kind of plan requires you to see an in-network provider unless it’s an emergency situation. Most require you to get a referral to see a specialist.

Preferred Provider Organization, or PPO, plans: This kind of plan allows you to see both in-network and out-of-network health care providers, although it typically is more expensive to go out of network.

Private Fee-for-Service, or PFFS, plans: This kind of plan allows you to see any Medicare-approved health care provider as long as they accept the plan’s payment terms and agree to see you, and you may also have access to a network of providers. You can see doctors that don’t accept the plan’s payment terms, but you might pay more.

Special Needs Plans, or SNPs: This kind of plan provides benefits to people with certain diseases, such as cancer, or health care needs, such as living in a nursing home. It also provides benefits to people with a limited income.

Medical Savings Account, or MSA, plans: These combine a high-deductible insurance plan with a medical savings account that can be used for health care costs.

Choosing between Medicare Advantage Plans will require you to understand your health care needs and think about what each type of plan offers. If you have a chronic health condition and you love your doctors, you’ll want health coverage that they accept. If you take prescription drugs, some plans may result in lower out-of-pocket costs than others.

Here are some questions to ask:

Do you have to get a referral? Some plans require you to get a referral from your primary care physician in order to see a specialist. If that’s not your preference, you’ll want to choose a plan with more freedom.

What benefits do they include? Do you need vision and dental coverage? Look for a plan that offers the benefits you want.

How much will your drugs cost? If you’re taking regular prescription drugs, compare costs within each plan to make sure you understand what you’ll be paying.

Are your doctors covered? If you like your providers, find out whether they’re included in the networks of the plans you’re considering.

What’s their rating? Each Medicare Advantage Plan comes with a star rating that ranges from one star to five stars. “I talked to a consumer in Massachusetts who essentially [won’t consider] any plan below a four-star plan,” Gordon says.

For additional help, try the Medicare Plan Finder on Medicare’s website.

How to switch Medicare Advantage Plans

If you’re already in a Medicare Advantage Plan, you can switch to a different Medicare Advantage Plan during either open enrollment period: Oct. 15 to Dec. 7, or Jan. 1 to March 31. After you join a new plan, you’ll be automatically unenrolled from your old plan once your new one starts.

Medicare Part B is outpatient coverage that helps pay for doctor visits and other medical services and supplies. It’s something most seniors rely on and those approaching age 65 look forward to.

» Learn what Medicare Part B covers

But it does come with costs. There are premiums, deductibles, copays and, in some cases, penalties. The more you know what to expect, the better you can plan for your health care costs.

What Medicare Part B will cost you

Premiums:

Most people pay a standard monthly premium for Medicare Part B: $148.50 in 2021. That figure rises with income, however. In 2021, beneficiaries whose 2019 income exceeded $88,000 (individual return) or $176,000 (joint return) will pay a premium amount ranging from $207.90 to $504.90, depending on income. See the table below for a breakdown.

2021 Medicare Part B premiums

Individual tax return (2019 income)

Joint tax return (2019 income)

Married & separate tax return (2019 income)

Monthly Medicare Part B premium

$88,000 or less

$176,000 or less

$88,000 or less

$148.50

$88,000 to $111,000

$176,000 to $222,000

Not applicable

$207.90

$111,000 to $138,000

$222,000 to $276,000

Not applicable

$297.00

$138,000 to $165,000

$276,000 to $330,000

Not applicable

$386.10

$165,000 to $500,000

$330,000 to $750,000

$88,000 to $412,000

$475.20

$500,000 and above

$750,000 and above

$412,000 and above

$504.90

Source: Medicare.gov

Deductible:

In 2021, the Part B annual deductible is $203. This is what you’ll pay before Medicare Part B coverage kicks in. The government usually adjusts the deductible amount each year.

Copays:

After you meet your deductible amount for the year, you will usually pay 20% of the Medicare approved amount of your bill. If your provider charges more than the Medicare-approved amount, your share of the bill may be more.

Penalty:

If you do not sign up for Medicare Part B during your initial enrollment period (the seven-month period starting three months before the month you turn 65) and you don’t have qualified insurance from another source, you’ll pay an extra 10% above the standard premium cost for every 12-month period you delayed. That extra premium can add up to a significant amount over the course of your retirement.

Medigap can help cover some costs

People who enroll in Original Medicare Part A and Part B often purchase Medicare Supplement Insurance, also called Medigap, to help pay for out-of-pocket costs. These policies often help with Part B copays or coinsurance, but they do not cover Part B premiums. Also, Medigap plans issued after Jan. 1, 2020, are not allowed to cover the Medicare Part B deductible.

Private insurers sell an array of standardized Medigap plans, with premiums regulated by the states. Your premiums may depend on where you live, what coverage you get and how old you are. Medigap plans are not used with Medicare Advantage plans.

The Medicare Advantage alternative

More than a third of people who sign up for Medicare choose a Medicare Advantage plan, also known as Medicare Part C.

» Learn how to compare Medicare Advantage plans

These policies, administered by private insurers, must provide the same coverage as Original Medicare. In addition, Medicare Advantage Plans may include prescription drug coverage and other benefits not included in Part A and Part B, such as dental and vision coverage.

Unlike Original Medicare, Medicare Advantage Plans often use a network of providers that plan members must use. In exchange, MA plans often cost less, with advertised premiums as low as $0 and limits on how much you will pay out-of-pocket. Be aware that in many cases, you will still have to pay the Medicare Part B premium.

Big data is playing a prominent role in life insurance this year.

Interest in coverage has surged during the pandemic, but for many people, social distancing mandates took the life insurance medical exam off the table. As consumers look for quick, noninvasive ways to buy policies, insurers have turned to accelerated underwriting, a process that uses algorithms instead of exams to evaluate applicants.

While accelerated underwriting isn’t new, more than a third of life insurers have expanded it due to the pandemic, according to a study by the Society of Actuaries. And no-exam life insurance appeals to many people. “They want it to be fast and easy,” says Gina Birchall, chief operating officer for the life insurance trade group LIMRA.

Accelerated underwriting can help you get life insurance quickly online, but there are caveats. What you gain in speed, you may lose in flexibility and price.

How big data has changed life insurance

Traditionally, buying life insurance was a lengthy process involving bloodwork, urine samples and long waits for approval. “It was probably the hardest or most difficult product to buy left in the modern economy,” says Brooks Tingle, president and CEO of John Hancock Insurance.

This changed as the world became steeped in big data. Insurers now typically check your prescription drug history and data from the MIB Group, an information-sharing service for insurers. Companies may also consider non-medical data, such as your credit history, driving record and shopping habits. Algorithms then combine these data points to quickly determine eligibility and cost of coverage.

This data can be tricky to dissect, but industry experts expect the trend to grow.

“The more information we have, the deeper the data that we have, the more capable we are of making sound decisions,” says Jackie Morales, chief insurance officer for Bestow, an insurer that uses accelerated underwriting.

How accelerated underwriting works

Companies typically use accelerated underwriting techniques in two ways:

To fast-track healthy people’s applications. Many major carriers approve low-risk applicants based on big data and then require medical exams for everyone else, says Jeremy Hallett, CEO of Quotacy, a life insurance broker. On average, it takes nine days for an insurer to reach a final decision using accelerated underwriting instead of the traditional 27, according to LIMRA. These policies are considered fully underwritten, even if you don’t take an exam.

To provide instant answers. Insurers like Bestow use information from your application and big data algorithms to assess risk, and never require a medical exam. Coverage is not guaranteed, but the application process is fast and you often get an answer within minutes.

Accelerated underwriting is not to be confused with “simplified issue” life insurance, which considers the answers on your application but doesn’t tap into big data. These policies typically cost more and offer less coverage than standard policies because they rely on limited information.

What to consider when choosing a policy

When you shop for life insurance, be sure to ask how the policy is priced. Both instant-answer and fully underwritten policies have pros and cons, and your specific needs will dictate what is right for you.

Before you apply, ask yourself these questions:

How fast do you want coverage?

If speed is paramount, consider instant-answer life insurance policies that solely use big data and never require an exam. You will get an answer quickly, although the answer may be no.

“What big data is providing people is speed,” says Bestow’s Morales. Nearly 85% of people who apply for a Bestow policy do so on a mobile device, she says.

How much do you want to pay?

A policy with full medical underwriting is likely to be the cheapest option. If the insurer chooses to use accelerated underwriting to fast-track your application, you are not penalized; your price and product will likely be the same as if you had taken the exam, Hallett says.

Instant-answer policies may not offer rates in the cheapest brackets since the insurer doesn’t have the option of a medical exam to get more information. But Morales says, “Some people will trade off that ability to get a fast decision at a reasonable price.”

Do you want flexibility?

Fully underwritten life insurance may offer more options, such as the ability to convert from term to permanent coverage. This is not always true of policies that rely solely on your application information and big data.

“When you at least have that medical exam as a possibility,” Hallett says, “you get a more robust product.”

This article was written by NerdWallet and was originally published by The Associated Press.

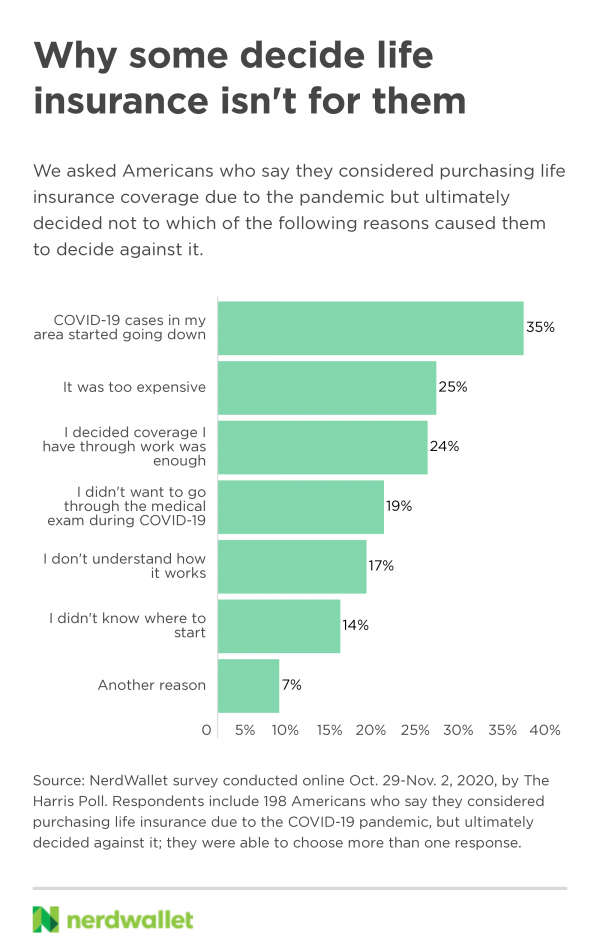

Perhaps fueled by acute awareness of their own mortality, many Americans shopped for life insurance during the pandemic. But some lost interest when local COVID-19 cases declined, a new NerdWallet survey found.

More than a third (35%) of those who considered purchasing life insurance due to the pandemic — but ultimately didn’t buy — say they decided against it because COVID-19 cases in their area started going down.

This behavior suggests some people view life insurance as a “panic purchase,” says Grant Dunn, vice president of financial services at Lakenan Insurance, a brokerage in Missouri. “That’s not what life insurance is made to do. It’s not meant to protect people for the next six months while COVID cases are high in their area. It’s meant to protect the family during all of your income-earning years and beyond.”

If the pandemic highlighted a hole in your coverage, you’ll likely need to address it regardless of how COVID-19 cases evolve. Learn how to determine whether you need life insurance, despite current events, and get the right coverage for you and your loved ones.

Why some shoppers decided against life insurance

Conducted online by The Harris Poll, NerdWallet’s survey asked U.S. adults who considered buying life insurance due to the pandemic, but ultimately chose not to, why they decided against it.

35% say their decision not to buy coverage was because COVID-19 cases in their area started going down.

25% say it was too expensive.

24% decided their workplace coverage was sufficient.

Whether you need life insurance, how much you should buy and how much you should spend are not easy questions to answer. In the survey, 17% of Americans who considered buying life insurance due to the pandemic but decided against it say it’s because they don’t understand how it works, and 14% say they didn’t know where to start. Unraveling these concerns can help you set up a more robust life insurance plan.

How to determine if you need life insurance

Immediate threats like the pandemic may highlight a need, but they shouldn’t dictate your buying decision. After all, an unexpected death could come at any time, not just due to COVID-19.

Similarly, just because you’re suddenly conscious of what you’d be leaving behind, it doesn’t automatically mean you need life insurance. Before you shop for coverage, ask yourself these questions:

Will your death create a financial burden?

You typically need life insurance if your death would place a financial burden on others. The type of burden is different for everyone. For example, you may need a large policy to support a spouse or children for several years, or a smaller one to cover final expenses, like burial costs.

A quick way to estimate the amount of coverage you need is to add up your long-term financial obligations and subtract your assets. Another popular rule is to multiply your income by 10. But these quick tricks are just a guide. Online calculators can help you determine how much life insurance you need.

Is the financial burden temporary?

How long other people will rely on you financially can dictate the type of life insurance you need. For example, if you’re supporting a child through college, consider a term life policy that covers only the years you need. Term life lasts a set number of years and is typically less expensive than permanent life insurance.

Alternatively, if you plan to support a family member for the foreseeable future, you might want to consider a permanent life insurance policy, as coverage lasts your entire life.

Is your workplace life insurance enough?

After calculating the amount of life insurance you need, check whether you already have sufficient coverage. In March 2020, nearly 6 in 10 American civilian workers participated in a workplace life insurance plan, according to data from the Bureau of Labor Statistics. However, group life insurance provided by an employer is generally one to two times your annual salary, which may fall short of what you need. And life insurance through work is typically tied to your employment, meaning if you lose your job, you may lose your coverage.

Ultimately, “life insurance is purchased for a need,” says Kathleen W. Bilderback, estate planning attorney at Affinity Law Group in St. Louis. “Someone can catch coronavirus and pass away, but someone can just as easily get in their car tomorrow and die in a car accident. So, if the need is there, the need is there.”

Among the 55% of Americans who say they have life insurance, a quarter say they purchased or increased life insurance coverage due to the COVID-19 pandemic, a NerdWallet survey finds.

The coronavirus pandemic has aimed a harsh spotlight on life’s precarity, and some Americans have responded by buying life insurance to provide their loved ones with financial support in the case of their death. According to a new NerdWallet survey, among the 55% of Americans who say they have life insurance — either through their workplace or an insurance company or broker — a quarter (25%) say they purchased or increased life insurance coverage due to the COVID-19 pandemic.

In a NerdWallet survey of more than 2,000 U.S. adults — among whom 1,078 have life insurance — conducted online by The Harris Poll, we asked about life insurance and why the pandemic inspired some Americans to get or increase coverage. We also examined why some U.S. adults thought getting life insurance was the right move and why others decided against it.

Key findings

Millions don’t have life insurance: About 2 in 5 Americans (39%) don’t have life insurance coverage, either through work or purchased from an insurance company. Another 7% aren’t sure if they have coverage.

COVID-19 inspires insurance sign-ups: One in 4 Americans who have life insurance (25%) say they purchased or increased their life insurance coverage due to the COVID-19 pandemic.

Younger Americans getting insured: Millennials (ages 24-39) who have life insurance are more likely than their older counterparts to have gotten or increased coverage due to the pandemic — 42%, compared with 30% of Gen Xers (ages 40-55) and 5% of baby boomers (ages 56-74).

Fear of and proximity to illness are motivators: For Americans who purchased or increased life insurance due to the pandemic, the top reasons for doing so were fear of being diagnosed with COVID-19 (30%) or knowing someone who was diagnosed with COVID-19 (29%).

Many cite dropping cases for dropping interest: Around 1 in 7 Americans who didn’t purchase life insurance through a company/broker (14%) considered purchasing life insurance due to the COVID-19 pandemic, but ultimately decided not to. More than a third of them (35%) say they decided against it because COVID-19 cases in their area started going down.

Parents, millennials get or increase coverage due to pandemic

The pandemic inspired some Americans to get or boost their life insurance. Of insured Americans, 13% say they purchased life insurance due to the COVID-19 pandemic, and an additional 12% say they increased their coverage because of it.

Parents of children under 18 are more likely to have life insurance than Americans without minor children (66% versus 50%). More than 2 in 5 insured parents of minor children (44%) say they purchased or increased their coverage due to the pandemic compared with just 13% of those without minor children. Insured millennials are more likely than their older counterparts to say they purchased or increased coverage due to the pandemic — 42%, compared with 30% of Gen Xers and 5% of baby boomers.

“The best time to purchase life insurance is when you’re young and healthy,” says Ben Moore, NerdWallet’s insurance specialist. “If you wait until you’re older or diagnosed with a chronic illness, premiums will be much higher.”

Fear of COVID-19 diagnosis biggest motivator for getting coverage

Among Americans who purchased or increased life insurance coverage in response to the pandemic, the biggest reason for doing so is a fear of being diagnosed with COVID-19 (30%). About the same proportion (29%) say they got or increased coverage because someone they know was diagnosed with COVID-19.

Close to 3 in 10 Americans who purchased or increased life insurance coverage due to COVID-19 (27%) say it’s because while they have life insurance through work, they felt it wasn’t enough. If you aren’t sure if your life insurance is sufficient, the amount of coverage you should get depends on several factors, including whether you have financial dependents, as well as your income and debt balances. You can use a life insurance calculator to determine how much coverage you should aim for.

Decline in COVID-19 cases leads to lessened interest in coverage

Around 1 in 7 Americans who didn’t purchase life insurance through a company or broker (14%) say they considered purchasing coverage due to the pandemic, but ultimately decided not to. Another 16% are still considering purchasing. For Americans who considered but ultimately opted not to get life insurance, the No. 1 reason they made that choice was that COVID-19 cases in their area started going down (35%).

A quarter of those who considered but ultimately decided against purchasing life insurance (25%) say it’s because it’s too expensive, and about the same proportion decided the coverage they have through work is sufficient (24%).

Among those who didn’t purchase life insurance, parents of children under 18 were much more likely than Americans without minor children to say they considered getting coverage due to the pandemic (52% versus 19%). Similarly, Black and Latino Americans who didn’t purchase life insurance are more likely than white Americans who didn’t buy to say they considered purchasing due to the pandemic (49% and 45%, respectively, versus 23%).

What uninsured or underinsured Americans can do

Consider your need for coverage, pandemic or not: While COVID-19 has certainly increased interest and urgency around life insurance, coverage is a good idea for many people, regardless of whether we’re experiencing a global pandemic. If anyone relies on your financial support, life insurance can provide that support if you aren’t around to do so. And even if you don’t have dependents relying on your income, life insurance can help your loved ones pay for end-of-life expenses such as funeral costs.

“If you were to die today, would there be a financial burden on someone else tomorrow? If so, then life insurance is probably a smart investment,” Moore says.

It’s also important to note that while fewer COVID-19 diagnoses in your area may provide you with some solace, cases have been ramping back up around the world.

Figure out what type of insurance is right for you: If you ultimately decide you want coverage, you’ll have to decide between term and permanent life insurance. Term life insurance lasts for a set period of time — say 10, 20 or 30 years — and pays out to your beneficiaries only if you die during said time frame. That means if you live longer than that, there’s no payout. However, it’s a more affordable option than permanent life insurance.

On the other hand, permanent life insurance covers you until the end of your life. There are several different types, including whole, universal, indexed universal and variable universal life insurance. Permanent life insurance is more expensive than term, but it builds cash value over time that can be used while the insured person is still alive.

“Term life is the most affordable option and will cover you until the kids have graduated or the house is paid down,” Moore says. “Permanent life is best if you need lifelong coverage and can afford the higher premiums.”

Learn how and where to start: Around 1 in 7 Americans who considered purchasing life insurance but decided against it (14%) say the reason why is that they didn’t know where to start. There are several factors you’ll want to consider when choosing a life insurance company, including cost of coverage, ability to pay claims and customer satisfaction. If you need help getting started, NerdWallet has rated the best life insurance companies, taking financial strength and any reported complaints about each company into account.

“The end of your life can be difficult to think about. But when you purchase a life insurance policy, you’re not only buying peace of mind, but also financial security for the people in your life who matter most,” Moore says.

Methodology

This survey was conducted online within the United States by The Harris Poll on behalf of NerdWallet from Oct. 29-Nov. 2, 2020, among 2,047 U.S. adults ages 18 and older. This online survey is not based on a probability sample and therefore no estimate of theoretical sampling error can be calculated. For complete survey methodology, including weighting variables and subgroup sample sizes

You probably need life insurance if your death would cause financial hardship to someone else. If the only coverage you have is through your job, though, you may not have enough.

Fortunately, buying life insurance has gotten easier in some ways during the pandemic. Plus, coverage may be cheaper than you think.

The rising COVID-19 death toll has led more people to at least think about their life insurance needs, and many have taken action. One in 4 Americans who have life insurance say they purchased or increased their coverage because of COVID-19, according to a NerdWallet survey conducted Oct. 29 to Nov. 2 by The Harris Poll. Many of those who purchased or increased their coverage were motivated by fear of being diagnosed with the disease (30%) or knowing someone who had (29%).

A survey by insurance industry trade group LIMRA this summer found nearly 6 in 10 Americans (58%) say they have a heightened awareness about the importance of life insurance, and about 3 out of 10 (32%) who were shopping for life insurance said it was in response to COVID-19. The number of term policies, the most popular type of life insurance, rose 10% in the third quarter compared with a year earlier, LIMRA found. That was the largest increase in 18 years.

“Obviously, the pandemic is making people much more sensitive to their mortality,” says Alison Salka, LIMRA research director. “So we see more people aware of the need for life insurance.”

Still, LIMRA has estimated that 30 million American households don’t have coverage, and another 30 million don’t have enough. The average coverage gap between what people have and what they need is about $200,000, LIMRA says.

“There is a perception about, ‘Well, I have it at work, and that’s got to be enough,’” says Marc Cadin, CEO of Finseca, another insurance industry group. “Most people have not done the work to really understand what would happen if they were to prematurely die.”

Employer-provided life insurance policies are typically capped at certain dollar amounts, such as $20,000 or $50,000, or limit coverage to one to two times an employee’s annual pay. That may seem like a lot, but parents with young children may need 10 times their salary or more to replace their incomes until the kids are grown. (Other types of insurance you may get from your employer, such as accidental death or critical illness policies, generally are too narrowly focused to protect you adequately.)

Even if your need is more modest — your partner requires your income to pay the mortgage, for example — an employer-provided policy might fall short. Plus, you typically lose your coverage if you lose your job, as many Americans have during the pandemic.

Having your own policy means your beneficiaries will remain protected. And thanks in part to the pandemic, you may be able to get coverage faster and without a medical exam.

Increasingly, insurers are automating and accelerating the application process, LIMRA’s Salka says. Instead of sending someone to your home to check vital signs and collect blood and urine specimens, some insurers are waiving exams or are exclusively using exam and lab data provided by the applicant’s physician. This trend was already underway, but social distancing and other pandemic challenges mean more insurers are adopting these practices, Salka says.

Life insurance is often cheaper than people expect, Cadin says. A 30-year-old woman in excellent health might pay $193 a year for 20-year term policy for $500,000. A 40-year-old man, also in excellent health, might pay $341 for the same coverage.

Term insurance covers people for a specified period of time, which is typically 10, 20 or 30 years. Term policies are significantly less expensive than permanent life insurance, which has additional features such as a cash value that can be borrowed against and that grows over time.

But the higher costs of permanent policies can tempt some buyers to skimp on coverage. If you do need life insurance — and you probably do if someone would be financially impacted by your death — then your priority should be getting enough.

How much is that? A life insurance calculator can help you refine your estimate. You may want to replace your salary for 20 or 30 years if your children are young, for example, and perhaps provide a college fund. You may want to add in your mortgage balance and any other debts. If you’re a stay-at-home parent or other unpaid caregiver, consider how much it would cost to hire someone to provide those services and for how many years. For example, your kids may need a full-time babysitter until they’re old enough for school and then a part-time one until they’re in their teens.

Once you have a total, subtract your “liquid” assets, such as savings accounts, college funds and any life insurance you already have. That’s the amount of life insurance you should start shopping for, without delay.

This article was written by NerdWallet and was originally published by the Associated Press.

Everything’s bigger in Texas, or so the saying goes, and unfortunately, that may include your renters insurance rates. The average cost of renters insurance in Texas is higher than the national average, but shopping around can often lower your rates. To help you narrow the options, NerdWallet compared companies across the state to find the best cheap renters insurance in Texas.

How much is renters insurance in Texas?

The average cost of renters insurance in Texas is $199 a year, or about $17 a month. That’s above the national average of $168 a year.

Tenants in the state’s two largest metro areas pay even more. Renters insurance in Houston costs $245 a year, on average, while tenants in the Dallas/Fort Worth area pay $194, on average.

» MORE: The best cheap renters insurance

Cheap renters insurance companies in Texas

NerdWallet analyzed rates across the state from a variety of companies to find the ones offering the cheapest Texas renters insurance.

Company

Average Annual Premium

Average Monthly Premium

Allstate

$108

$9

The Hartford

$132

$11

Nationwide

$160

$13

Mercury

$167

$14

Guard

$174

$15

Amica

$181

$15

UPC Insurance

$199

$17

Texas Farm Bureau

$208

$17

Republic Group

$210

$18

State Farm

$231

$19

Farmers

$237

$20

Texas FAIR Plan Association

$241

$20

Progressive

$242

$20

USAA*

$96

$8

*USAA is available only to military, veterans and their families.

More about some of the cheapest companies

Allstate: You can get a variety of discounts on an Allstate renters policy, including up to 20% for having no claims history and up to 25% for being at least 55 years old and retired.

The Hartford: This company partners with AARP to offer renters insurance primarily to older Americans. The Hartford will waive its renters insurance deductible up to $5,000 for certain major claims worth $27,500 or more.

Mercury: If you live in a gated community, have smoke alarms, or have both auto and renters insurance with Mercury, you could save money on your renters policy.

Nationwide: Along with standard coverage for liability and personal belongings, Nationwide renters insurance also includes coverage for expenses due to theft like unauthorized credit or debit card transactions and forged checks.

Texas FAIR Plan Association: Created by the Texas government, the FAIR Plan Association is the state’s insurer of last resort, offering coverage to those who have been turned down by at least two other companies. Although it’s not the cheapest option in Texas for renters insurance, it is the only option for some tenants.

USAA: Unlike most insurance companies, USAA includes coverage for flood damage as part of its renters policies. But only veterans, active military and their families can buy USAA renters insurance.

» MORE: The best cheap car insurance in Texas

Cheap Texas renters insurance from the best companies

If you’re looking to buy insurance from widely available companies with a strong reputation, consider one of the following insurers from NerdWallet’s list of best renters insurance companies.

Company

NerdWallet rating

Annual premium

Allstate

4.0NerdWallet rating

$108

The Hartford

4.0NerdWallet rating

$132

Nationwide

5.0NerdWallet rating

$160

Amica

4.5NerdWallet rating

$181

State Farm

5.0NerdWallet rating

$231

Farmers

4.5NerdWallet rating

$237

USAA*

5.0NerdWallet rating

$96

*USAA is available only to military, veterans and their families.

What to know about Texas renters insurance

Natural disasters, such as tornadoes and tropical storms, happen regularly in Texas. If one strikes your home, your landlord’s insurance will cover only the building structure, not any damage to your possessions. That’s why it’s important to know what’s covered (or not) when shopping for renters insurance in Texas.

Flooding is the state’s most common disaster, according to the Texas Department of State Health Services, but it’s not covered by standard renters policies. If you’re at risk — for example, if you live in a ground-floor apartment near the beach or another low-lying area — you may want to purchase separate flood insurance.

Renting a place on the Gulf Coast? Make sure your renters insurance covers damage due to hurricane and tropical storm winds. Though many standard renters policies cover wind-related claims, such coverage may be specifically excluded if you live in high-risk areas near the coast. The Texas Windstorm Insurance Association is operated by the state and offers wind and hail policies to those who can’t find coverage elsewhere.

» MORE: Hurricane prep: What Texas renters need to know

Even if you’re not in an area prone to hurricanes, you may still want extra wind coverage. More than 100 tornadoes strike the state each year, on average.

Wildfires are another common disaster in Texas, and while most renters policies cover losses due to fire, you’ll want to make sure you have enough personal property coverage to replace all your belongings if the worst happens. The calculator below can help you estimate how much your possessions are worth.

What determines Texas renters insurance rates?

You may pay more or less than the average annual premiums listed above, depending on various factors.

Your location. If you live on the Gulf Coast where hurricanes are common, or in a neighborhood with a high crime rate, you may pay more for a renters policy.

Your credit. Many insurance companies use a credit-based insurance score — similar to a traditional credit score — to evaluate how likely you might be to file a claim. People with better credit tend to get cheaper renters insurance rates.

Your claims history. If you’ve filed any renters insurance claims in the past few years, your insurer may charge more for your policy.

Your coverage limits. If you have more possessions — or particularly valuable possessions — to cover, you’ll typically pay more for renters insurance.

Your deductible. Raising your deductible is an easy way to lower your Texas renters insurance premium, as long as you feel confident you can access enough cash to pay it if necessary.

Other policies. If you buy your renters and auto insurance from the same company, you can often get a bundling discount.

Your home’s features. Home security systems, fire alarms and 24-hour building security guards could earn you discounts.

Your dog. Dog bites are a common cause of renters liability insurance claims, so if your pup is a breed that insurance companies consider high-risk, such as a pit bull or Doberman pinscher, your premium might be higher (if the animal is covered at all).

» MORE: Renters insurance quotes: What you need to know

Texas Department of Insurance

If you have questions, concerns or complaints about your renters insurance, the Texas Department of Insurance may be able to assist. You can call its consumer helpline at 800-252-3439 for service in both English and Spanish.

When you buy or renew a renters policy in Texas, your insurance company is required to give you a copy of the department’s Consumer Bill of Rights for renters insurance. This document is worth a read: It explains how Texas insurance companies can use your credit information, establishes timelines for claims processing and lists circumstances under which your policy can and can’t be canceled.

Though it’s increasingly legal, marijuana can still raise red flags for life insurance companies. While some insurers don’t mind covering you if you use pot, others will charge you higher rates or deny your application outright.

About 22.2 million Americans use marijuana every month, according to the Centers for Disease Control and Prevention. It’s now legal for medical use in 36 states and for recreational use in 15, as well as for both in Washington, D.C.

If you’re one of the millions of Americans who use marijuana and you’re looking for a life insurance policy, you can probably find coverage. You may need to shop around, however, as companies don’t view the risks that weed poses to long-term health in the same way.

Can marijuana users get life insurance?

In a word, yes, you can get life insurance if you use marijuana. In fact, life insurance may not cost more for some marijuana users than for those who don’t use it at all — depending on the insurance company and other factors.

Every insurer measures risk differently. Most consider factors like age, gender, weight and family health history. Some may look at your hobbies, such as mountain climbing or skydiving. Your history of drug use, whether marijuana or otherwise, can also come into play.

If you use marijuana, companies will likely consider how often and why you use it, according to Quotacy, a Minneapolis-based life insurance brokerage. If there’s a medical reason, the insurer will want to know about the condition you’re treating.

Because each company has different standards, you may need to research several insurers before you find one willing to cover you at a reasonable price. You can also work with a life insurance broker or agent who is experienced with marijuana use and can shop the market for you.

How do life insurance companies view marijuana use?

When applying for coverage, you’ll have to answer questions about your lifestyle and in many cases take a life insurance medical exam that may include drug testing.

“Keep in mind, if the application process includes a blood test, the marijuana usage might turn up in the results,” said Adam Weinberg, brand director for Haven Life Insurance, in an email.

Be sure to tell the truth about your use before taking your test. Lying on a life insurance application can result in an automatic decline for coverage. You also run the risk of your insurer refusing to pay your death benefit to your loved ones if it finds out later that you lied on your application.

When you apply for life insurance as a marijuana user, there are three potential outcomes:

You’re declined outright.

You’re approved at a tobacco rate, even if you don’t use tobacco. Rates for cigarette smokers and other tobacco users are typically several times higher than what a healthy applicant who doesn’t use tobacco might pay.

You’re approved at a non-tobacco rate.

While some studies have shown marijuana to be less harmful to the lungs than tobacco smoke, smoking is still smoking — meaning it’s less healthy than not smoking at all. And even if you don’t smoke but choose to vape or eat your weed, the jury is still out on how bad it is for you long-term.

“We don’t have a crystal-clear vision of how marijuana affects mortality because it has been illegal, so getting people to admit it — and doing the studies that an actuary needs — have been challenging,” says Jeremy Hallett, CEO of Quotacy.

How will marijuana use affect your rates?

When insurers decide whether to sell you a policy and how much to charge, they generally don’t consider whether marijuana is illegal where you live, Hallett says — but they do pay attention to how often you indulge. Occasional use of pot may not affect your rate much, if at all, while more frequent use could lead to higher premiums or even a denial.

Chris Abrams of Marijuana Life Insurance, an independent agency in San Diego, provided sample rates to show how typical marijuana habits can affect monthly insurance premiums. Abrams’ hypothetical applicant is a 30-year-old man, in excellent health, applying for a $500,000, 30-year term life policy.

Never uses marijuana: $30 a month.

Twice a year: $31.

Once or twice a week: $55.

Two to three times a week: $62.

Four times a week: $126.

Six times a week: $166.

The breaking point appears to be more than six times per week for recreational users. Very few insurance carriers will offer standard, non-tobacco rates to daily pot users, according to Hallett.

For most companies, Abrams says, “daily use is a ‘decline.'”

Does using marijuana mean you’ll lose your life insurance?

If you already have life insurance and you decide to give marijuana a try, don’t worry — it won’t affect an existing policy.

“Once you’re underwritten at a point in time for your insurance, that is your rate,” Hallett says. “The carrier can’t come back and raise your rates. You’re good to go.”

Medicare generally doesn’t cover the cost of residing in assisted living communities, which are facilities that offer housing and custodial services — such as laundry, cooking and managing medications — for older adults. However, it does cover care received at skilled nursing facilities, which are equipped to provide more medical care than assisted living communities, when certain requirements are met.

If you move to an assisted living community, Medicare will still cover your approved prescriptions, surgeries, doctor’s appointments, screenings and medical equipment, just as it did when you lived at home.

Assisted living community vs. skilled nursing facility: What’s the difference?

Assisted living communities, which are in residential settings, aren’t the same as nursing homes or skilled nursing facilities, which are in clinical settings.

Nursing homes offer a greater level of medical care and may be eligible for Medicare coverage in certain cases. Assisted living communities generally focus on providing custodial care, such as bathing, eating, meal preparation, getting dressed or using the bathroom. Original Medicare (Part A and Part B) doesn’t include coverage for custodial care when it’s the only care you need.

»MORE: What is Medicare, and what does it cover?

In some cases, a company might operate both an assisted living community and skilled nursing facility in the same building or a neighboring one, under the same name. The coverage you receive through Medicare depends on which care you’re receiving and whether you meet certain requirements.

In order to get Medicare coverage for skilled nursing care:

You must have just had a qualifying hospital stay and not used up all your covered hospital days.

Your doctor must determine that you need this care.

Your current condition is either the reason you were just hospitalized, or it developed as a result of your being in the hospital (for example, an infection you picked up while hospitalized).

This skilled nursing care must be considered medically necessary.

If you meet all these conditions, you would be 100% covered for the first 20 days in residential care, then be responsible for $185.50 per day in coinsurance for days 21 through 100. After 100 days Medicare doesn’t provide any coverage for this type of care.

What about Medicare Advantage?

Medicare Advantage (Medicare Part C) must cover at least as much as Original Medicare. But since Medicare Advantage is private insurance contracted through the government, the specific benefits of each policy are unique.

That said, Medicare Advantage doesn’t typically cover assisted living or any other long-term custodial care, although it continues to cover your eligible medical expenses like prescriptions, surgery, doctor’s appointments, screenings and equipment if you move to an assisted living facility. It may also provide some additional benefits such as transportation to your medical appointments, vision and hearing coverage and gym memberships.

Also like Original Medicare, your costs may be covered if you need short-term care at a skilled nursing facility immediately following a hospitalization.

Assisted living costs and how to pay

The national median cost for residential care at an assisted living facility was $51,600 per year in 2020, according to a survey from Genworth, a major provider of long-term care insurance.

»MORE: What will you spend on health care costs in retirement?

In general, if you have long-term care insurance, your policy will usually cover these costs if you meet certain requirements. If you don’t have this type of coverage, you may have to tap into savings or home equity to cover costs.

When to enroll in assisted living

Moving to an assisted living community is a huge step, both financially and emotionally. If you’re unsure about whether this is an appropriate option, here are a few clear signs that assisted living might be right for you:

It’s getting hard to care for yourself. Cooking, eating and after-meal cleanup may feel like so much work that your nutrition suffers and you experience unhealthy weight loss. Maybe you’ve been skipping showers due to fear of falls, not washing clothes as often as you should because the laundry basket is too heavy, or having difficulty bending to put on socks and shoes.

It’s getting hard to care for your home. Perhaps it feels too strenuous to vacuum, scrub and declutter, and your house isn’t meeting your standards of cleanliness anymore.

It’s difficult to get around, even at home. Getting in and out the bathroom, up and down the stairs, or even out of bed in the morning may have become an issue.

Assisted living communities also may have minimum age requirements; for example, some are limited to residents 62 and older.